How much longer can the debt-burdened consumer hold up the U.S. economy?

If the American consumer is Atlas — holding up “the greatest economy ever” — his legs are weakening under the strain.

The following article was originally published in “What I Learned This Week” on October 10, 2019. To learn more about 13D’s investment research, please visit our website.

In the Trump era, two seemingly contradictory narratives have dominated the portrayal of U.S. consumers. On one hand, you have the tale of the indefatigable American consumer — Atlas holding up “the greatest economy ever.” On the other hand, there’s the inequality-crippled majority — the bottom 90% squeezed by wage stagnation and a rising cost of living, one unexpected expense from debt-driven ruin, and looking for a savior to fix the rigged system, whether Trump, Bernie Sanders, or Elizabeth Warren.

The problem is, both narratives are true. Through August, retail sales had increased for six straight months, the longest stretch since 2017. With the trade war dragging on capital spending and exports, the U.S. economy’s reliance on the consumer has escalated dramatically this year.

Yet, if the consumer is Atlas, his legs are weakening under the strain. Consumer debt has surged to nearly $14 trillion or roughly 19% of GDP, surpassing the total of 17.5% prior to the Global Financial Crisis (chart below). Not including mortgages, millennials now carry an average of $27,900 in debt, according to analysis released by Northwestern Mutual last month. For Gen Z — the oldest of whom are still only 22 years old — that number is an incredible $14,700. As for baby boomers, they have just under $137,000 saved for retirement on average, far less than needed to support current spending.

As recessionary threats mount, cracks are becoming apparent in consumer fortunes and confidence. The manufacturing recession has begun to tip over into services. Wage gains have begun to fall. And higher prices loom as the U.S.-China trade war escalates. As Deutsche Bank’s Torsten Slok warned last month: “The fundamentals for consumers are more worrying than we think.”

No industry better illustrates the American consumer’s precarious support for the economy than the auto industry. As we explored in WILTW June 6, 2019, the average price of a new vehicle in the U.S. has soared 29% since 2009 to a little over $36,000. These price increases have largely insulated the U.S. auto industry even as car sales have begun to decline globally. Yet, the way American consumers are paying for pricier new cars suggests unsustainability.

Americans held a record $1.3 trillion in auto-related debt at the end of June, nearly double the amount a decade ago. Meanwhile, loans have been stretched to allow greater short-term affordability, as The Wall Street Journal reported last month:

“The median-income U.S. household with a four-year loan, 20% down and a payment under 10% of gross income — a standard budget — could afford a car worth $18,390, excluding taxes, according to an analysis by personal-finance website Bankrate.com.

But the size of the average auto loan has grown by about a third over the past decade to $32,119 for a new car, according to Experian. To keep payments manageable, the car industry has taken to adding more months to the end of the loan.

The average loan stretches for roughly 69 months, a record…As a result, a growing share of car buyers won’t pay off the debt before they trade in their cars for new ones, either because the car is in need of repairs or because they want a newer model. A third of new-car buyers who trade in their cars roll debt from old vehicles into their new loans, according to car-shopping site Edmunds. That is up from about a quarter before the financial crisis.”

Credit card debt — which currently totals roughly $1 trillion in the U.S. — is also showing signs of vulnerability. In the second quarter, commercial banks charged-off 3.74% of all credit card loans against their reserves at a seasonally-adjusted annual rate, the fastest rate of bad-debt write-downs since 2012.

Yet, even as consumers have struggled to keep up with credit-card burdens, they’ve still piled on more debt. July’s consumer spending — which increased a seasonally adjusted 0.6% versus June — inspired widespread optimism that a recession wasn’t imminent. As Jack Kleinhenze, chief economist at the National Retail Federation, told the WSJ in August: “The consumer is still very sturdy and providing fundamental strength to the overall economy.”

That optimism appears misguided given the spending was debt-fueled to an extreme. As NBCNews reported last month:

“According to the Federal Reserve’s consumer credit tracker, revolving credit — a category in which credit card debt predominates — increased at an annualized rate of 11.25% in July, the most recent month for which data is available. ‘In terms of revolving debt, we see spikes like this every so often, but they don’t jump by double digits all that much,’ said Matt Schulz, chief industry analyst at CompareCards. Typically, big jumps occur around the holidays, though — not in July.”

Lower interest rates are unlikely to provide meaningful relief for credit-card burdened consumers. According to September analysis by WalletHub, average credit card APRs for people with good credit sat at 20.9%, the highest since the personal finance platform began tracking rates in 2010. Based on calculations by CompareCards, for borrowers with $6,000 in credit card debt making monthly payments of $250, even a half-percentage-point rate cut from the Fed would save only between $63 and $72 off their total debts.

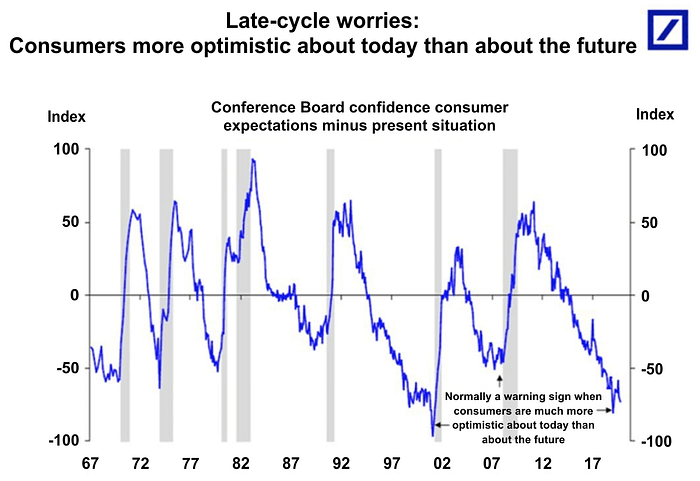

With consumers stretched, volatility returning to markets, the trade war ever-present in headlines, and recessionary indicators flashing, consumer sentiment has begun to sour. As Slok warned in a recent letter to clients, consumers confidence that tomorrow will be better than today has plummeted.

Personal consumption expenditures edged up only 0.1% in August, a sharp deceleration compared to the first seven months of the year when spending increased at a monthly average of 0.5%. The savings rate hit 8.1%, up from 7.8% in July. And then last month, U.S. services-sector activity expanded at its slowest pace in three years. It appears consumers have begun belt-tightening in preparation for an economic slowdown.

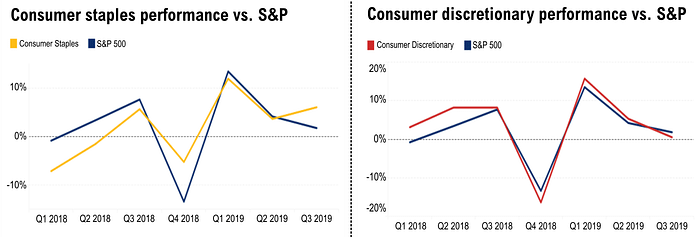

Markets are clearly underestimating the threat of a consumer spending slowdown. Consumer staples and discretionary indexes have both outperformed the broader market YTD, advancing 18% and 16.1%, respectively, versus 15.2% for the S&P 500.

Both indexes now trade at a premium to the broader market. As CNBC reported last week:

“Compared to the 2019 price earnings ratio for the S&P 500 of 17.5 today, the average staple stock trades at 22 times with the average consumer discretionary priced at a turn of 23 on this year’s earnings per share…The market pays a premium for growth. Do we really believe that most of the packaged food, consumer brands, and traditional retailers are deserving of a premium?”

Despite a decades-low unemployment rate, wage growth fell to 2.9% in September, down from 3.2% in August. Meanwhile, a range of new tariffs on Chinese goods are set to go into effect in mid-December, threatening a significant tax on consumer spending. “Roughly 60% of the estimated $160 billion of imports scheduled to be implemented on December 15 will be computers and other electronic devices,” according to Syracuse economics professor Mary Lovely. Estimates suggest these tariffs could cost the average American family anywhere from $1,000 to $2,000 annually.

Mortgage, credit card, and auto default rates are relatively low and stable, giving many pundits reason to believe the U.S. consumer remains strong. All-important Christmas-season spending will show how much optimism the consumer has left. But as Dallas Fed chief Rob Kaplan told Rana Foroohar of The Financial Times recently: “If you wait to see weakness in the consumer, you’ve likely waited too long.”

This article was originally published in “What I Learned This Week” on October 10, 2019. To subscribe to our weekly newsletter, visit 13D.com or find us on Twitter @WhatILearnedTW.